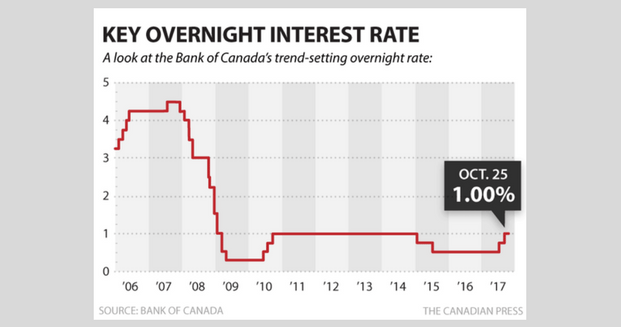

The Bank of Canada has decided not to increase it’s key overnight interest rate at it’s October meeting. In the wake of Canada’s economic success, the Bank of Canada has recently chosen to increase interest rates twice. Now at 1 percent — still a historic low — this interest rate level appears to be here for some time. The Bank of Canada, headed by Governor Stephen Poloz, does not appear to be interested in aggressively pushing rates upwards. Rather, it will likely now give the market more time to stabilize before further adjustments are made.

It was expected by some market analysts that the next interest rate increase could occur in January at the latest. Now it is more likely that a new interest rate increase will happen in March of next year.

The Bank of Canada has had Canadian interest rates at an artificially low set point for some time, designed to encourage spending and improve the countries overall economic outlook. Now that Canada’s economy is flourishing, the Bank of Canada is likely to continue to increase rates until they are at normal levels — it’s only a matter of time.

The Canadian dollar did weaken slightly in the wake of new interest rate announcements, after which many investors had decided to hold off on new investments and purchases until they had more information regarding future interest rates. Policy makers are undoubtedly concerned that continuing to increase interest rates could further strengthen the dollar — and could consequently have a negative impact on the economy as a whole.

That does not mean that interest rates are not going to rise, as these historically low interest rates were never expected to last this long.

What does this mean for the real estate market? In terms of the real estate market, buyers may have a little more time to get into the market before the Bank of Canada begins to push rates past their current 2008 recession levels. Both buyers and sellers may want to consider entering the market sooner rather than later, as once interest rates do increase, buyers will have less spending power. This comes at a time when new mortgage rules may also be limiting pools of buyers.

Buyers will find that now is the best time to get into the market. Buyers who are on the cusp of affordability may very well be priced out of the market by new interest rate increases — and buyers who are holding on for “the right time” could find themselves with severely limited buying power.

For now, it appears that the Bank of Canada wants more time to see the impact of the last two interest rate increases. They recognize canadian consumers, real estate purchasers, and investors sensitivity to these interest rate changes, and the Bank of Canada is doing what it can to minimize economic impact. At this time it looks like rate increases will be on hold until the spring. This is good news but should not be used to justify any hesitation about getting into the market. Both tighter mortgage underwriting rules and higher interest rates mean that buyers and sellers should act swiftly.